GBR

GBR How well has GSK Assessed the Risks of their Product Development and Sales to Maximise Shareholder Value

| ✓ Paper Type: Free Assignment | ✓ Study Level: University / Undergraduate |

| ✓ Wordcount: 4665 words | ✓ Published: 27th Feb 2020 |

Executive Summary

This report provides an analysis and evaluation on how Glaxo Smith Kline (GSK) assessed the risks of their product development and sales with respect to their ability to maximise shareholder value. Methods of analysis include dividend pay-out ratios, buy backs, share prices and sales growth. Agency theorists (1980s) believed that the market allocation of resources was more efficient than managers allocation. The established literature on shareholder value and financialization considers the impact of the stock markets’ increasing demands for financial returns on corporate behaviour, governance and performance (Froud et al, 2002; Andersson et al, 2007). Results of data analysed show that GSK is a perfect example of financialization since, it assessed risks of their product development and sales in the name of shareholder value. The company claims that high prices are being used to incentivise innovation, but the profits are being used to create short term returns to investors. The recommendation includes how GSK should find a healthy balance between short and long-term goals as it is crucial for the sustainability of the core business. This report will be focusing on GSK from the mid-1990s to recent events. The report will focus on the expiration of Zantac and M&A following on to recent events to have a wider view. To summarise, this report will firstly analyse the pharma industry and the blockbuster business model, where marketing expenditure is more regarded than research. This report will also analyse how the Zantac blockbuster provided organic growth, but then the business model is unsustainable. Secondly, an examination in inorganic growth created by M&A to overcome lack of innovation. Thirdly, an observation into different strategies in maintaining equity return to investors while searching for a new blockbuster in the pipeline. Finally, this section will present how research is undervalued by investors and how GSK manage those pressures by incentivising the CEO with compensations based on performance.Pharmaceutical Industry

GSK’s mission statement: “our quest is to improve the quality of human life by enabling people to do more, feel better and live longer” (AMBS, 2018). In the pharmaceutical industry, there are 2 reputational opinions. The good pharma believes that R&D should lead to the recycling of profits to sustain innovation, which offers the social benefit of improved health. On the other hand, bad pharma believes that the industry is market driven and makes large profits from the exploitation of the sick. Ethical drugs offer high margins of profit, but also create strong year-on-year growth as they can charge premium prices for drugs which helps to recoup costs from R&D. Intellectual property rights, excludes competitors from muscling in and protects prices, margins and creates a monopoly of power. However, those rights are time-limited patents; The Food and Drug Administration (FDA) limits the patentable life of a drug to 14 years from the point of approval. The US has the highest drug prices in the world due to the large uninsured population and cost-sharing requirements for those with coverage are more burdensome than in other countries (D. O. Sarnak, 2017). UK Prescription Price Regulation Scheme data for 1996 through 2010 show that, US drug prices were between 74% and 181% higher than the UK. (Lazonick, et al., 2017). The high prices imposed by large pharmaceutical companies has been criticized by Senator Estes Kefauver, Chairman of the United States Senate's Anti-Trust and Monopoly Subcommittee indicated that patents sustained predatory prices, excessive margin costs and prices are increased due to large expenditures on marketing(Rahman, 2018). This contrasts with pharmaceutical companies that claim that price regulations will kill innovation. GSK on patents; “we support intellectual property protection because it stimulates and fundamentally underpins the continued R&D (GSK, 2002). At the same time, there was a rapid growth in prescription drugs prices from 1990, when the average cost per prescription drug was $27.16 compared to $65.29 in the 2000s (Froud, et al., 2006) According to Balance et al. (1992) raising prices were the industry’s response to the broader problem of decelerating medical discoveries.Business Model: Blockbuster Model

The Blockbuster business model refers to the method of spending large amounts of money in R&D, in the hope of creating a successful blockbuster that will generate annual sales of over $1 billion. The objective is volume sales of blockbuster drugs as a basis for cost recovery and aggressive marketing to build blockbuster sales. Zantac, Glaxo’s most successful blockbuster was launched in 1983 in the USA. It captured the anti-ulcerant therapeutic segment from 1982 to 1997, contributing more than 50% of overall sales revenue in 1989 and more than 30% of overall sales revenue between 1985 and 1995 (AMBS, 2018). Zantac provided year to year organic growth to Glaxo and high returns. The market value of the company increased by 2092.59% from 1982 to 1997 (refers to Appendix 1) as a result of an extraordinary increase in sales. In 1988, there was a maximum increase of 28.1% in return on sales. The success of Zantac was an increase of dividends from 10% of sales revenues in the 1980s to 15% per cent by 1994 (AMBS, 2018). Blockbusters do not simply happen, they must be created through a combination of scientific and marketing efforts. As a result of the Zantac success, by 1992 there were 2.5 marketing employees for every person engaged in R&D (Froud, et al., 2006). Glaxo’s sales gains were reallocated to 37% on marketing compared to 13% on research by 2000 (AMBS, 2018). The stock market is interested by developments in forthcoming promising products which could produce another successful Blockbuster. Glaxo knew that the loss of patent in Zantac will reduce the extraordinary sales due to competition replicating the product. Glaxo responded with an increase in R&D expenditure, from 6.1% in 1982, when Zantac was launched, to 15.2% by 1994. Despite this, no new blockbuster drug emerged that could feasibly replace the losses on sales after the Zantac patent expired. Glaxo’s limited spend on R&D and massive spend on marketing was an intelligent response to increase shareholder value but by no means sustainable. The balance between R&D and marketing reflects the long stability of the business and the short-term profiteering where managers under pressure forfinancial results will lean more on marketing rather than developing new products. Appendix 2 shows that from 1980 there was an increase in dividend pay-outs, but by 1992 Glaxo profits were lower than the company’s dividend pay-out. This is in line with shareholder-value-driven management, where managers' decisions are emphasised to improve financial results (Froud, et al., 2006). Blockbusters are highly risky due to the expiring time frame of patents and the consequence of a large decline in sales stemming from aggressive competition. This is called a “patent cliff”. The lack of innovation is a huge barrier to discover new blockbusters (Kandybin & Genova, 2012). Even though Pharma companies increase their R&D expenditure few get results. It is also a long-term game, it typically takes a decade from the time a drug is discovered to being prescribed by doctors. This situation is unsustainable. Companies facing declining revenues and a more cautious regulatory regime can no longer keep spraying cash around in the hope of finding a blockbuster (Stovall, 2011).Mergers and Acquisitions (M&A); Wellcome and SmithKline Beecham

The expiry of the Zantac patent posed a huge threat to Glaxo as sales of the drug fell 84% by 2002. Horizontal mergers offer cost reduction and improved positioning when cost recovery falters (Froud, et al., 2006). In 1995, the Wellcome acquisition bought some time for GSK as they began gutting the newly acquired company in order to reap the benefits. Immediately after the merger the company let go two thirds of Wellcome’s employees. Subsequently R&D expenditure decreased from 993m in 1993 to 542m by 1996 (AMBS, 2018). Despite this, the share price rose from $8.11 in 1994 to $23.52 by 2000 as the market believed that the acquisition represented not so much an event as a formula that Glaxo management could subsequently repeat (Froud, et al., 2006). According to The Economist (2000) it was clear that buying Wellcome was an interim solution with only short-term savings and, no long-term growth. A second deal with SmithKline Beecham (SKB) by 2000 allowed Glaxo to diversify into new therapeutic areas and expand further into the lucrative US market. After the merger, GSK had a total of 43,000 sales representatives, including 8,000 in the USA, which gave it the largest US sales force in the industry. The merger immediately brought an increase in sales of 114% in the more lucrative US market, compared with 52% in Europe. The merger also allowed Glaxo to extend its portfolio of blockbuster products such as Avandia. The addition of SKB did not improve a relatively weak pipeline due to SKB having a similar lack of innovation when producing new drugs as they themselves had only one blockbuster since 1995 (Froud, et al., 2006). After the SKL merger, it was more difficult for Glaxo to convince investors that the merger was a solution to its pipeline problems. The return on capital employed (ROCE) decreased from 58% to 100% range produced in 1995-9 after acquisitioning Wellcome from 43% to 53% after the SKL merger. Additionally, share prices decreased from £18.63 at the end of 2000 to £12.80 by the end of 2002. Furthermore, despite low profitability in 2001 and 2002 dividend payments were higher; with $703m and $2,057m of retained profit net compared to $2,097m and $2,356m of dividend payments. This suggests that Glaxo is trying to retain investor confidence even though it may have to dip into their retained profits from previous years. With these fundamental performance issues, Glaxo may find such financial strategies to be unsustainable and detrimental to the profits of the firm, as augmented in the “shareholder value” theory (Froud et al. 2000). These M&As reflect Glaxo industry’s desire to avoid the imminent danger of the patent cliff, rather than an interest in enhancing R&D capabilities.Avandia

In May of 1999 the FDA approves Avandia for regulating blood sugar, created by SKL. After 1 year, the two companies merged to form GSK. In 2001, at the FDA’s request, GSK commissioned a large study comparing cardiovascular outcomes of Avandia to other commonly-used diabetes medicines. The results of GSK’s study showed no links between Avandia and heart disease (Thomas, 2013). That same year GSK spent extra expenditure on lobbying from $4m compared to $2.92m the year before (refer to Appendix 3) and research expenditure dropped significantly (AMBS, 2018). In 2004 GSK was caught hiding data showing side effects of the antidepressant paroxetine in children: a court settlement required them to make public all clinical trial results. Using this data source, cardiologist Prof Steve Nissen published a landmark meta-analysis in 2007 showing a 43% increase in the risk of heart attack on rosiglitazone. The FDA found a similar risk in their own calculations but voted in 2007 to keep the drug on the market. The same year Nissen published an updated meta-analysis of 56 trials on over 35,000 patients, which found an increased risk of heart problems. GSK claimed that since 2007, their seven trials showed no excess risk. GSK also stated they looked at 164 trials, although these trials lasted no more than four weeks. Regularly trials of this nature would last over 24 weeks as heart risk takes time to develop (Goldacre, 2010). GSK was also holding back data from academics and doctors. Finally, the FDA restricted the use of Avandia in 2010 after Dr. Graham, an FDA scientist, found as many as 100,000 heart attacks, strokes, heart failure and deaths linked to Avandia since it came on the market in 1999 (Freeman, 2010). The U.S. Senate Finance Committee in 2008 released a report accusing GSK of intimidating physicians, suppressing critics and hiding negative data while marketing the drug. GSK has been charged with $3.49bn to cover costs relating to a U.S. investigation of its marketing practices, as well as additional costs tied to consumer lawsuits over the health damage produced by the drug (Whalen, 2011). After 8 years on the market, Avandia sales plummeted from a $3bn peak to $680 million in 2010. GSK’s response to this scandal was to double its share buyback program to $25 billion, boosting its shares even though sales of Avandia dropped greatly (Reuters, 2007). GSK knew that their share price would decrease, therefore a massive buyback would make the GSK equity more attractive to compensate for the scandal. This clearly demonstrates that management focused on shareholder value rather than the ethics and reputation of the company.Diversification

Diversification from their Core Business through Consumer Products

In 2008, GSK organised its scientists into small teams called drug performance units (DPUs) and instructed them to research different diseases. Mark Dainty at Citigroup said: " Creating smaller teams may help companies to better innovation and decision-making in the long term. Whether it delivers greater returns is a whole other question." (Stovall, 2011). Financial institutions, which held large amounts of GSK equity were unhappy with the company’s emphasis on long-term growth, as changes to R&D takes years to have a revenue impact. For instance, JPMorgan (2008) recommends selling the stock as a consequence of CEO Andrew Witty’s announcement of the share buyback programme, which delayed creating room for business development activities. Blockbuster drugs require much more in-depth research and development. Therefore, GSK selling higher volumes with lower margin type like consumer products can diversified risk and provide regular return to shareholders. In 2011, GSK and Dentsply agreed to create a portfolio of oral care products, known as Sensodyne. According GSK’s annual report (2017), consumer healthcare turnover was £7,750m (GSK, 2017). In GSK’s case, rather than continuing R&D for better drugs and better products, they are focusing on their shareholders whilst at the same time making smaller, less-risky products such as toothpastes.Expansion to China

One way of avoiding the challenge of rigorous regulations has been through diversifying into emerging countries as pointed out by Kefauver (1952). GSK’s new strategy was to focus less on high-priced products and place greater emphasis on high-volume sales of products for the emerging world. China is the world’s largest pharmaceutical market after the U.S, with sales worth $116.7bn in 2016 (FT,2018). Investors agreed with this strategy as shares were still up by 20% and investors could take comfort in the company's diverse global business. The company posted a pre-tax profit revenue of £7.6bn. It returned £6.3bn to shareholders through dividends and share buybacks over 2013. Sales in China were £759m, up 17% over the previous year (Petroff, 2013). China has a different culture and local regulatory requirements; bribery and corruption are simply expected as a way of business. For instance, it is common practice for hospitals to have systems in order to divide the profits from the bribes. “China’s ministry of public security in July accused GSK of being the “godfather” of a network of corruption involving up to $500m in bribes paid by company officials to doctors” (Ward & Waldmeir, 2014). GSK responded by scrapping individual sales targets for commercial staff in China. Michael Hewson (2013) said “There will be a bit of collateral damage on the share price, then people will move on, both parties need one another." (Petroff, 2013)Corporate Governance

William Lazonick (2014) argues that the only logical explanation is that stock-based compensation gives senior executives personal incentives to do buybacks to boost stock prices. Stock awards realised gains depending on the market price of the stock on the date that the award vests (Hopkins and Lazonick 2016). CEO Witty’s share options in 2011 were; 196,634 awards which have vested and 297,421 awards which have lapsed (Alliance news, 2014 ). According to GSK’s annual report (2011), it paid dividends of £3.4bn and spent £2.2bn on repurchasing shares, compared to £4bn on R&D. Option incentives led to managers focusing on short term equity return rather focusing on R&D to ensure the long-term stability of the business (Lazonick & O’Sullivan, 2000).Competitors

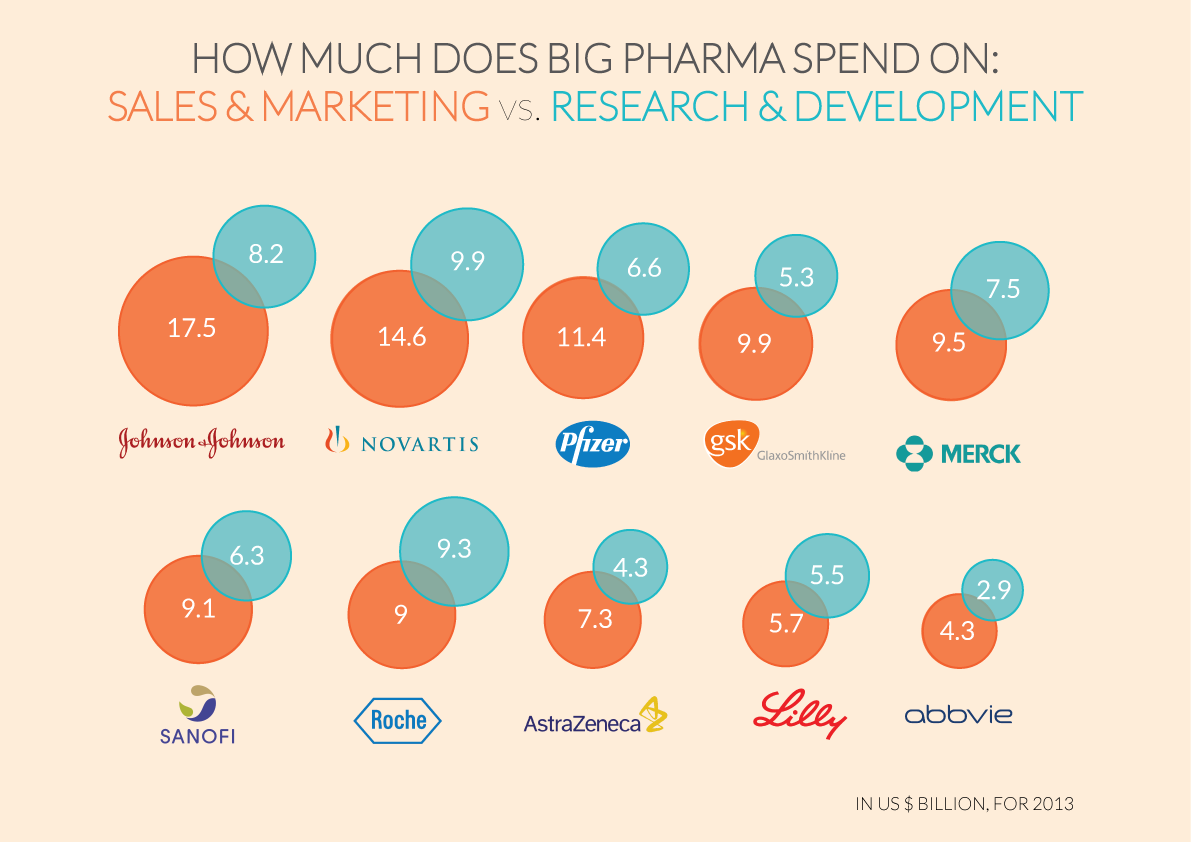

In hindsight, GSK has certainly seen a decline relative to its competitors. In 2000, GSK was the biggest pharma company in the world by revenues. By 2018, Roche is now the world’s leading pharma company, with GSK languishing at number 9 (refer to Appendix 4). Unlike GSK, Roche has greater expenditure for research over sales and marketing (refer to Appendix 5). GSK claims that pharmaceuticals and R&D remain its strategic focus and yet the fact remains that the company’s R&D spending is low compared with its rivals (Nicholls, 2018). Appendix 6 shows that GSK’s market returns are underperforming compared to the average pharma industry for the past 5 years. Furthermore, GSK P/E ratio of 38.92 is lower compared to 39.5 ratio of UK pharma companies.Conclusion

GSK assessed risks of their product development and sales to ensure short term shareholder value. Planning the future of the company to create long term results seemed not viable for GSK, as they continually underinvested in R&D. After Zantac, GSK’s strategies have provided inorganic growth as the company has been existing off patented drugs with very little to replace them in the pipeline. GSK’s claims of wanting to improve people’s lives by investing in R&D, but profits from high prices are being used to maximise shareholder value. GSK is a perfect example of financialization defined by Krippner (2005), where companies concentrate more on profits created from financial channels rather than their core business. Profits are being allocated in dividends paybacks and buybacks for the sole purpose of giving manipulative boosts to their stock prices. Managers are being incentivized with stock-based compensation that rewards senior executives for stock-price “performance”, to create short term return instead of long-term growth for the business. Agency theorists are certain that managers attempt to maximize their own personal wealth through risk management, however this leads to underinvestment in R&D that could improve the company’s perspective value.Recommendations

This report recommends that GSK needs to keep a healthy balance short-term equity return and long-term stability for the business. Managers need to focus more on the core business, since it shows during the M&A period, if the core business is not working, financial performance is not either. GSK needs to focus more on their long-term stability such as having new drugs in the pipeline which will require higher research expenditure.Appendices

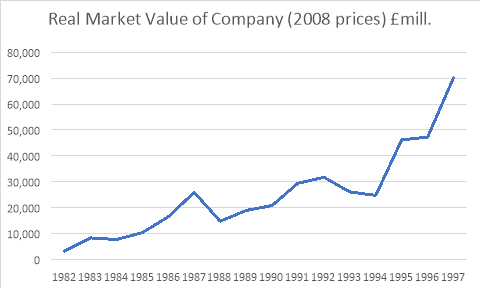

Appendix 1

Percentage increase from 3,202m in 1982 to 70, 207m in 1997= 2092.59% increase in market value.Data taken from AMBS, 2018. GSK spreadsheet, Manchester : University of Manchester.

Percentage increase from 3,202m in 1982 to 70, 207m in 1997= 2092.59% increase in market value.Data taken from AMBS, 2018. GSK spreadsheet, Manchester : University of Manchester.

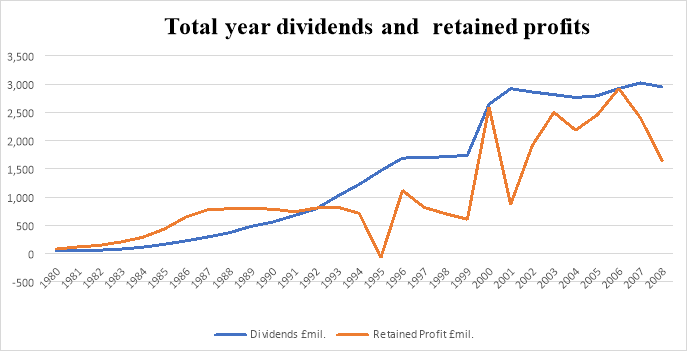

Appendix 2

Data taken from: AMBS, 2018. GSK spreadsheet, Manchester : University of Manchester.

Data taken from: AMBS, 2018. GSK spreadsheet, Manchester : University of Manchester.

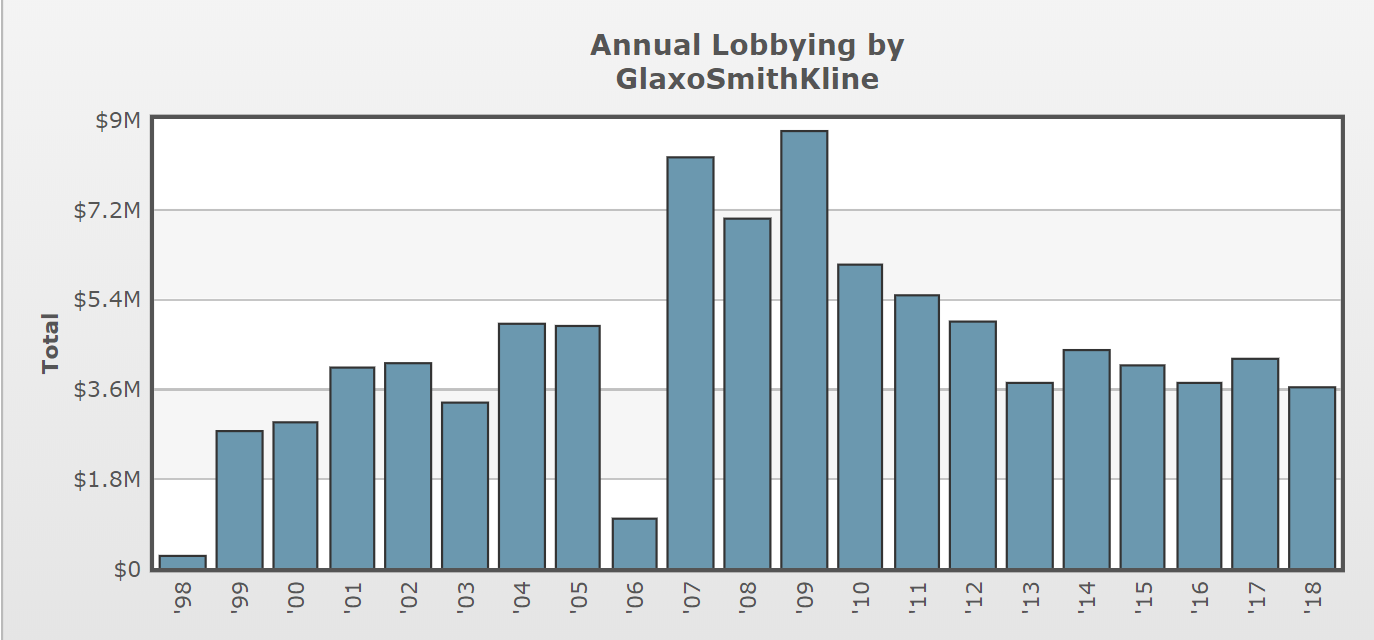

Appendix 3

Graph taken from: Center for responsive politics , 1999. opensecrets. [Online]

Available at: https://www.opensecrets.org/lobby/clientsum.php?id=D000000133&year=1999

[Accessed 5 December 2018].

Graph taken from: Center for responsive politics , 1999. opensecrets. [Online]

Available at: https://www.opensecrets.org/lobby/clientsum.php?id=D000000133&year=1999

[Accessed 5 December 2018].

Appendix 4

Picture taken from: Rahman, S. A., 2018. Lecture 11, International Business Analysis Project. Power point document Available at: AMBS University of Manchester

Picture taken from: Rahman, S. A., 2018. Lecture 11, International Business Analysis Project. Power point document Available at: AMBS University of Manchester

Appendix 5

Picture taken from: Rahman, S. A., 2018. Lecture 11, International Business Analysis Project. Power point document Available at: AMBS University of Manchester

Picture taken from: Rahman, S. A., 2018. Lecture 11, International Business Analysis Project. Power point document Available at: AMBS University of Manchester

Appendix 6

| GSK shareholder return | ||||||

| 7 day | 30 day | 90 day | 1 year | 3 year | 5 year | |

| GSK | 1.4% | -6% | -1.1% | 12.6% | 12% | -4.5% |

| GB Pharma | -2.1% | -3.3% | 1.6% | 15.4% | 22.3% | 26.5% |

| Data point | Value |

| Earnings per share | £0.38 |

| GSK share price | £14.79 |

| P/E ratio | £14.79/0.38=38.98x |

| P/E ratio pharma companies (Median) | 39.5x |

Bibliography

Abraham, J. & Reed, T., 2001. Trading risks for markets: The international harmonisation of pharmaceuticals regulation,. Health, Risk & Society, , pp. 113-128.Alliance news, 2014 . DIRECTOR DEALINGS: GlaxoSmithKline Executives Share Awards Vest. [Online] Available at: http://www.morningstar.co.uk/uk/news/AN_1392400149667412000/director-dealings-glaxosmithkline-executives-share-awards-vest.aspx [Accessed 5 December 2018].AMBS, 2018. GSK Case Pack, Manchester: University of Manchester .AMBS, 2018. GSK spreadsheet, Manchester : University of Manchester .Center for responsive politics , 1999. opensecrets. [Online] Available at: https://www.opensecrets.org/lobby/clientsum.php?id=D000000133&year=1999 [Accessed 5 December 2018].Cooper, C., 2015. Independent. [Online] Available at: https://www.independent.co.uk/life-style/health-and-families/health-news/glaxosmithkline-a-drugs-giant-that-puts-the-lives-of-the-poor-before-the-money-of-the-rich-could-it-10237538.html [Accessed 13 December 2018].D. O. Sarnak, D. S. G. K. a. S. B., 2017. Paying for Prescription Drugs Around the World: Why Is the U.S. an Outlier? , s.l.: The Commonwealth Fund.Deutsche Bank , 2008. Deutsche Bank Glaxo Report, s.l.: s.n.Freeman, D. W., 2010. Diabetes Drug and Risk: Avandia Linked to Stroke, Heart Trouble, Deaths. [Online] Available at: https://www.cbsnews.com/news/diabetes-drug-and-risk-avandia-linked-to-stroke-heart-trouble-deaths/ [Accessed 12 December 2018].Froud, J., Johal, S., Leaver, A. & Williams, K., 2006. Financialization and Strategy. s.l.:Routledge.Goldacre, B., 2010. Diabetes drug 'victory' is really an ugly story about incompetence. The Guardian.Goldacre, B., 2012. Bad Pharma; how drug companies mislead doctors and harm patients. 4th ed. London: Fourth Estate.GR, K., 2005. The financialization of the American economy. Socio-Economic Review , p. 173–208.GSK, 2011. GSK Annual report 2011, s.l.: GSK .GSK, 2017. Annual report 2017, s.l.: GSK.GSK, 2017. Annual report 2018, s.l.: GSK.Igeahub, 2018. Igeahub. [Online] Available at: https://www.igeahub.com/2018/03/06/top-10-pharmaceutical-companies-2018/ [Accessed 3 December 2018].JPMorgan , 2008. JPMorgan Glaxo, s.l.: s.n.Kandybin, A. & Genova, V., 2012. Big Pharma’s Uncertain Future. [Online] Available at: https://www.strategy-business.com/article/00095?pg=all [Accessed 25 November 2018].Lazonick, W., Hopkins, M. & Ken Jacobson, 2017. US Pharma’s Financialized Business Model. Institute for new economic thinking, Volume Working Paper No. 60, p. 29.Lazonick, W. & O’Sullivan, M., 2000. Maximizing shareholder value: a new ideology for corporate governance. Economy and Society, Volume 29, pp. 13-35.Miller, E., 2018. Drugwatch. [Online] Available at: https://www.drugwatch.com/avandia/ [Accessed 26 November 2018].Miller, E., 2018. Drugwatch. [Online] Available at: https://www.drugwatch.com/avandia/ [Accessed 3 December 2018].Nicholls, A., 2018. Pharma Times. [Online] Available at: http://www.pharmatimes.com/magazine/2018/june_2018/is_trouble_on_the_horizon_for_gsk [Accessed 11 December 2018].Petroff, A., 2013. CNN. [Online] Available at: https://money.cnn.com/2013/07/17/investing/gsk-china-risks/index.html [Accessed 11 December 2018].Rahman, S. A., 2018. Lecture 11, International Business Analysis Project. [Online] Available at: AMBS University of Manchester [Accessed 12 December 2018].Reuters, 2007. Glaxo Doubles Buyback to $25 Billion as Earnings Flatten. CNBC , 25 July .Stovall, B. S., 2011. Glaxo Scientists Brush Up on Sales Pitches; By Making Scientists Pitch For Development Funds,. The Wall Street Journal , 11 October .Thomas, C., 2013. The Ethical Nag; Avandia: a very short history of a very bad drug. [Online] Available at: https://ethicalnag.org/2013/01/21/avandia-a-very-short-history-of-a-very-bad-drug/[Accessed 12 December 2018].Ward, A. & Waldmeir, P., 2014. Financial times. [Online] Available at: https://www.ft.com/content/1ee62c8e-b406-11e3-a102-00144feabdc0?siteedition=uk#axzz3GcAwBeM5 [Accessed 3 December 2018].Whalen, J., 2011. Glaxo to Take $3.49 Billion Litigation-Risk Charge. The Wall Street Journal , 18 January .

Cite This Work

To export a reference to this article please select a referencing stye below:

Reference Copied to Clipboard.

Reference Copied to Clipboard.

Reference Copied to Clipboard.

Reference Copied to Clipboard.

Reference Copied to Clipboard.

Reference Copied to Clipboard.

Reference Copied to Clipboard.

Related Services

View all

DMCA / Removal Request

If you are the original writer of this assignment and no longer wish to have your work published on UKEssays.com then please: